Is the Supercharged 3.21% Nov Singapore Savings Bond a Buy?

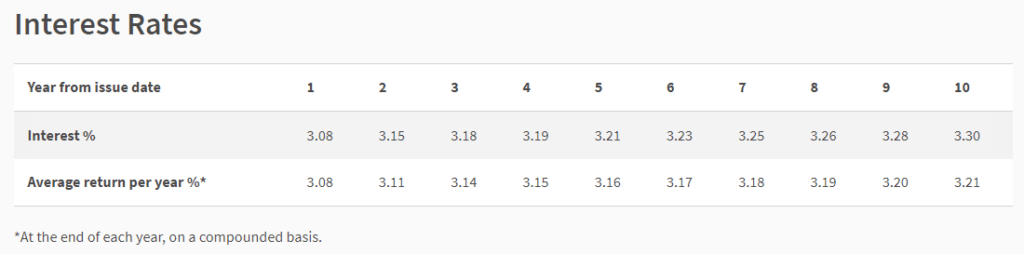

Most markets are drowning in a sea of red but there is at least one piece of good news to start the month. The 10-year average return for the November issue of the Singapore Savings Bond (SSB) has climbed to 3.21% – the highest level recorded since its inception in October 2015. This is 0.21% higher than the previous 10-year average return peak of 3%, which was recorded just in August 2022.

Nov SSB Offers Record High Short- And Long-Term Rates

In addition to the headline 10-year average return of 3.21%, the 1st year return of 3.08% is also a record high. This is excellent because one gets to earn relatively high return in the first year (first few years even) whilst waiting for opportunities to “upgrade” to higher new SSB issues. I will elaborate more on this later.

As you can see in the graph in the top picture, the Singapore benchmark government bond yields across 1 – 10 year maturities have rose and converged over the past year. A slightly more sophisticated way to describe this is “the yield curve has flattened”. SSB interest rates are required to “step up” (increases) each year to attract investors to hold it as a long-term investment, but a flattish “step up” ladder means this attraction is greatly diminished.

Singapore Interest Rates Will Rise Further but Likely Lag the U.S.

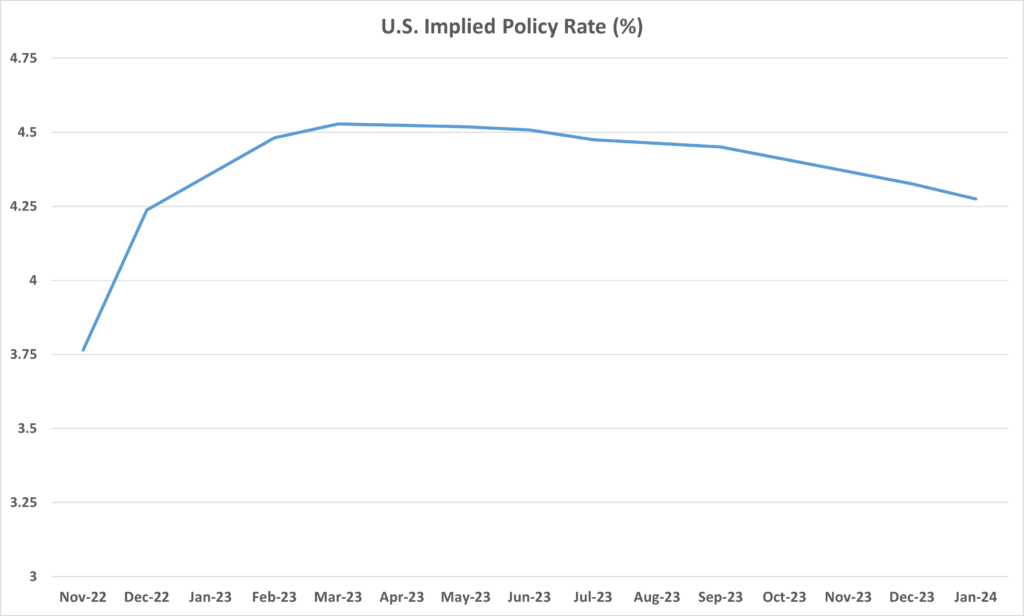

The US federal funds rate (target interest rate at which commercial banks borrow and lend their excess reserves to each other overnight) is now at 3 – 3.25%. Futures contracts tied to the Federal Reserves’ policy rate showed on 30 Sep 2022 that benchmark U.S. interest rates will peak in Mar 2023 at about 4.5%. The implied fed funds rate declines gradually to 4.275% in Jan 2024.

Singapore interest rates is expected to follow the U.S. higher. Historically, the pace of increases in Singapore were less drastic than the U.S. and it is playing out the same way in 2022 so far.

SSB Offers Flexibility for Free Upgrade

One would not lose money investing in SSB unless the Singapore government defaults. This is because SSB redemption is done at par (receive back 100% of the amount invested). Therefore, for the remaining months till maturity of the existing SSB, if a new SSB can provide higher returns over those months then one can do a “free upgrade”!

Do take note that you need to have excess cash to invest in the new issue before the closing date at the end of the month (9pm on 26 Oct 2022 is the closing for Nov 2022 issue), as cash from the redemption of existing SSB will only be returned early in the following month (01 Nov 2022 for current redemption).

SSB pays interest every 6 months. If you redeem your bond when there is a scheduled interest payment, you will receive the scheduled interest together with your redemption amount. If you redeem before the scheduled interest is paid, you will receive a pro-rated amount, called the accrued interest, which is the interest you have earned but have not been paid.

A useful resource I found is http://www.ilovessb.com/swap which calculates the profit/loss for swapping existing SSB with new one. I cannot vouch for the accuracy for this website so use it at your own risk. So far, the results are quite close to my own calculations.

Expect Oversubscription Again

SSB issues since June 2022 have been oversubscribed. The maximum amount offered has been increased in the past few months to the latest $900 million, but I expect November 2022 SSB issue to be oversubscribed again with the 10-year average rate above 3% for the first time.

So, Is Nov SSB a Buy?

Yes, in my view. SSB is a safe and liquid instrument, offering flexibility and in recent months higher returns. Despite the “Bond” name, you are not bonded by it if interest rates rise, and should in fact upgrade when opportunities arise. I continue to treat SSB together with the increasingly attractive T-bills as a Bond + Cash hybrid part of my portfolio. Do refer to the SSB website for more details.