Can You Boost Your CPF OA by Investing in T-bills?

Thank you for reading Relak Investor’s first post!

With rising interest rates, I understand that some Singaporeans are thinking of boosting their CPF Ordinary Account (CPF OA) by investing in T-bills. The idea is intuitive – buy T-bills using idling CPF OA savings as yields are now higher than CPF OA interest rate of 2.5%. There is no additional risk as T-bills are debt securities issued by the Singapore Government. Is this really a free lunch? Let us do a deep dive.

CPF OA Interest Rate Is Unlikely to Rise Above 2.5%

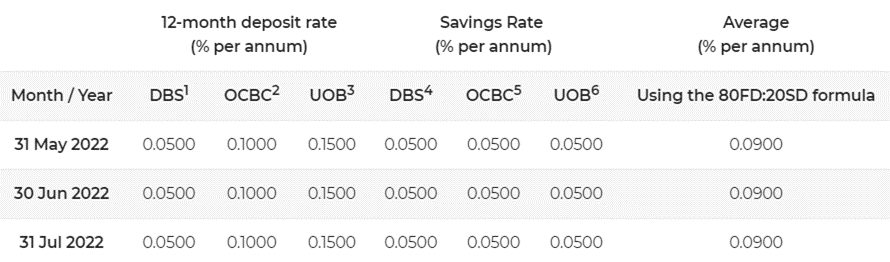

Reviewed quarterly, the CPF OA interest rate is computed based on the 3-month average of major local banks’ interest rates (80FD:20SD formula). This computed rate is only 0.09% for the latest period from May 2022 to July 2022, which will apply for 1 October 2022 to 31 December 2022. I am glad that the CPF OA interest rate is subjected to the legislated minimum of 2.5%!

The 12-month deposit rates used for this computation are the “basic” rates, not “promotion” rates which are much higher. As of 1st October 2022, OCBC’s “basic” 12-month deposit rate is 0.10% while the “promotion” 12-month deposit rate is 2.6%. Therefore, CPF OA interest rate is unlikely to rise above 2.5% even if fixed deposit rates continue rising, unless the formula changes.

What Are T-bills?

There are four types of Singapore Government Securities: Treasury Bills (T-bills), SGS bonds, Singapore Savings Bonds (SSB) and Cash Management Treasury Bills. Only the first three types are available to individuals, and only the first two types can be bought with CPF funds. You can find a detailed comparison on the MAS website.

T-bills are shorter term with maturities of 6 months or 1 year whereas SGS bonds are longer term with maturities ranging from 2 to 50 years. Currently, 6-month T-bills are issued every fortnight, 1-year T-bills are issued every quarter, and SGS bonds for different maturities are issued a couple of times in a year. Do refer to the MAS Auctions and Issuance Calendar for the exact dates.

T-bills have grown in popularity amongst retail investors in recent months with rising interest rates. Short-term yields (6-month to 2-year) has risen from about 0.5% in 2021 to more than 3% now. In the US, they have risen from near zero in 2021 to around 4% now!

The Opportunity Cost of CPF Investing

CPF interest is computed monthly and compounded annually. Banks typically calculate savings account interest based on the average balance of the month, but CPF calculates interest based on the lowest balance of the month. This means that withdrawals or deductions made during the month will not earn interest in that given month. Also, contributions and refunds received during the month will only start earning interest next month.

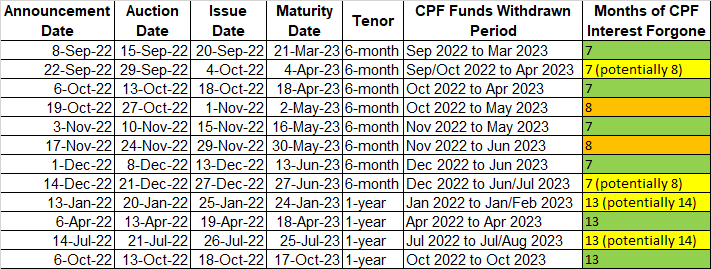

The opportunity cost of using CPF savings for investments is that it does not earn CPF interest during the investment period. I have estimated the number of months of CPF interest forgone based on the issue date and maturity date for selected past and upcoming T-bills issues in the table below.

The actual deduction from CPF OA takes place after the auction date and before the issue date. Thus, I will avoid issues with issue date and maturity date near the start / end of the month. Issues around the middle of the month are safer in this aspect. Hereon, I will assume 1 month of “forgone” CPF interest in the examples and calculations since we have the choice on which issue to buy.

How Much Are the Extra Returns?

Let us take a closer look at an example of a 1-year T-bill with a 3.3% yield, which is around the current MAS 1-year benchmark yield.

- CPF interest forgone: $100,000 * 2.5% * 13 months / 12 months = $2,708.33

- Yield earned from 3.3% T-bill: $100,000 * 3.3% * 12 months / 12 months = $3,300 (so extra $591.67 earned over 1 year)

- Expressed differently, Extra Returns = Amount invested * [ {SGS % yield * M / 12} – {2.5% * (M+1) / 12} ] where M = tenor of T-bill or SGS bond in months

As a reference, the breakeven yield is the T-bills or SGS bonds yield where I would not earn or lose anything for using CPF OA to purchase T-bills or SGS bonds. Obviously, I require a higher number than these to make my effort worthwhile.

- Breakeven for a 6-month T-bill: 2.5% * 7 / 6 = 2.92%

- For a 1-year T-bill: 2.5% * 13 / 12 = 2.71%

- For a 2-year SGS bond: 2.5% * 25 / 24 = 2.60%

Competitive or Non-Competitive Bid

SGS are issued via a uniform-price auction. Investors will need to select either Competitive Bid or Non-Competitive bid.

For Competitive Bid, you will invest in the bond only if it yields above a certain level (up to 2 decimal places). For example, if you have other investment options and will not accept anything less than 3.10%, then you can put a Competitive Bid at 3.10%.

- If the cut-off yield eventually ends up at 3.30%, you (and everyone else being allotted successfully) will get full allotment at 3.30%

- If the cut-off yield eventually ends up at 3.00%, you get nothing

- Lastly, if the cut-off yield eventually ends up at 3.10%, you will get a pro-rata allotment

For Non-competitive Bid, you do not need to specify the yield and will be accepted at the cut-off yield of successful competitive applications, with pro-rated allotment if applications exceed 40% of amount offered. Non-competitive bids will be allotted first, up to 40% of the total issuance amount, and a glance at recent issues shows that 100% of Non-Competitive applications are allotted every time.

An important thing to note is that those who are successful (both Competitive Bid or Non-Competitive Bid) are allotted the securities at the SAME cut-off yield, which is the highest accepted yield of successful competitive bids.

More Considerations

My impression is that banks, financial institutions and large funds are the main ones using Competitive Bid and thus sets the cut-off yield. Non-Competitive Bid users are usually price takers who are not particular about the exact yield.

For my cash investments, I have used Non-Competitive Bid as I know what the recent benchmark yields (published daily) are and I am happy to invest at similar levels. The cut-off yield should not be too far off from the recent benchmark yields. However, for CPF investments, I think it is better to use Competitive Bid and set a yield of your choice taking into account the “minimum” breakeven yields discussed previously.

Process and Other Considerations

You will need a CPF Investment Account with one of the three CPFIS agent banks (DBS/POSB, OCBC, and UOB), and submit an application in person at any branch. As with all investments using CPF OA, there are small $2-2.50 per transaction and quarterly service charges depending on the bank. They are not significant and can be ignored.

Applications typically close a day before the auction date, and banks may stop CPF OA applications even earlier, so do not wait until the last minute.

My Plan

Based on current SGS short-term yields of around 3.3%, I think it is still somewhat marginal NOW to spend the time to visit the bank branch to apply. However, the interest rate futures market is pricing in more rate hikes by the Fed up to a peak of around 4.5% to 4.75% in the middle of 2023. Unlike long-term yields which are harder for the Fed to control, short-term yields are highly influenced by the Fed funds rate. It will be wise to monitor for the next few months and consider opportunities to boost your idling CPF OA savings if SGS short-term yields do reach above 4%.

Amongst the maturity options, I think the 2-year SGS bond is the best deal as one month of foregone interest is spread over a longer maturity period compared to the 6-month and 1-year T-bills. Visiting the bank branch every 6 months is no fun! The 5-year or 10-year SGS bond are too long for me, in case I need the CPF OA savings for a house purchase in the near future. The potential challenge is that 2-year SGS bonds were only issued twice this year.

Summary

Taking a step back, I think we have to carefully consider what our plans are for any idling CPF OA savings. Some of us may be keeping it for a house purchase in the near future or even as a contingency for monthly housing instalments. Equities are markedly down this year so another consideration is whether one has plans to deploy CPF OA savings into equities.

Feel free to reach out to me directly here if you have any queries!